Drivers and Enablers for Moving Ahead of the Competition

By: Lisa Kennedy

Tom Singer

Kevin Hume

Tompkins International

August 2013

Introduction

Final delivery is not new, but new drivers and enablers are changing its role and importance. The process of final delivery has been disrupted by the creation of omnichannel operations, through competition, endless aisle, and same-day/next-day delivery. This process begins when an order is placed, by a consumer to a retailer, or to a consumer products company doing retail, or to an endless aisle supplier, or to a distributor. This order process can vary: telephone, text, online, tablet, smartphone, or email with a request for the item to be delivered directly, within a timeframe as defined by the consumer.

There is a need for a new model that calls for a strong online sales focus with omnichannel strategies to keep pace with changing customer expectations.

Final delivery services are not new to consumers, and the direct-to-consumer B2C and B2B delivery model is already established for other industries. Examples of consumer-accepted final delivery can be found in services like in pizza delivery, floral delivery, and delivery of automotive parts to a mechanic.

Companies have found a way to successfully deliver inexpensive items directly to a consumer at reasonable rates. Retailers like Gap, Inc. have fulfilled orders from their e-commerce websites for direct-to-consumer delivery for years.

However, some retailers built on home delivery have yet to become mainstream. Consider online grocery shopping companies such as Peapod. While successful, they have not really become as prevalent as service models like pizza delivery. The Peapod example can tell us a great deal about consumer expectations.

Why has a service like Peapod not yet reached a high level of market saturation? A few possibilities:

-

Too expensive for consumers to afford, with its $7-10 delivery fee.

-

Lengthy delivery times, as the fastest delivery window is next-day.

-

Lack of flexibility, due to the requirement of a minimum $60 order.

-

Availability of competitors, such as the number of other grocers per square mile.

-

A lack of market penetration meant too few orders within a delivery zone, which drives up costs that are then passed on to the consumer.

How can retailers, consumer product companies, endless aisle suppliers, and distributors achieve a different result, and instead establish successful final delivery in direct-to-consumer sales? To serve customers, delivery costs must be reduced and delivery times decreased.

However, what worked yesterday won’t work tomorrow. Customer expectations and competition are rapidly changing the face of final delivery. Standard ground service is no longer acceptable in many segments. Next-day and same-day services are becoming the norm. Limited availability and backorders have given way to endless aisle selection. There is a need for a new model that calls for a strong online sales focus, with omnichannel strategies capable of keeping pace with changing customer expectations.

The New Retail Model

The new retail model is online, but with a focus on omnichannel operations, which include direct-to-consumer delivery on the customers’ terms.

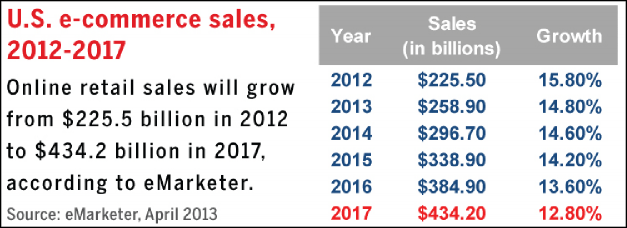

This model incorporates online, because of how Amazon has driven B2C and B2B consumers to buy more online, drawing them in with options and experiences that they prefer. Internet retailing is expected to almost double from $225.5 billion in 2012 to $434.2 billion in 20171. The chart below shows exponential sales in e-commerce in the US. These sales will directly affect the volume of goods shipped through final delivery services.

Although there will be a mix of in-store pick-up and direct-to-consumer delivery, the missing puzzle piece is how to get orders to the consumer on-time and cost-effectively. The success factor to really grow online sales is finding ways to reduce delivery costs while decreasing the delivery window.

These ways include store fulfillment, leveraging local carrier and courier services, and providing other options besides home delivery, such as pick-up and drop-off (PUDO) lockers and in-store consumer pick-up.

1 eMarketer, April 2013.

This white paper looks at the drivers and enablers of final delivery. Drivers include online and omnichannel retailer competition, the need for endless aisle, and movement to quicker fulfillment. Enablers include network design, order management, store fulfillment systems and final delivery service providers (local, regional and national).

Driver: Online and Omnichannel Retailer Competition

E-commerce has permanently changed the retail landscape. A brick and mortar retailer’s average sales per square foot peaked in 2007 at $4542. By the end of 2009, the average had fallen to $401. Omnichannel retailers have now embraced e- commerce, and now compete head to head with online retailers.

Omnichannel retailers now realize that new customer acquisition and store traffic are often driven by their online offerings. In fact, Sak’s, Inc. has said that over 50% of all their sales are influenced by their online presence. Consumers who order online now have several options to get their orders.

The obsolescence of the traditional e-commerce model (online orders delivered to homes from a fulfillment center) is driven by two critical business strategies geared to increase market share:

-

Endless aisle. This is the ability to offer products for sale where no inventory is held by the retailer. The inventory is held by a supplier and shipped after receiving the order from the consumer. Endless aisle requires the capability to view inventory availability everywhere (including suppliers) and ship product from anywhere. Systems are the foundation of inventory visibility, distributed order management (DOM), and downstream store fulfillment. To date, these systems have been lacking sophistication to support endless aisle, but technology is advancing. Endless aisle offers the ability to deliver products from anywhere (stores, forward fulfillment centers, DCs, suppliers) which are no longer sourced around a large remote DC. This allows for more available inventory and puts retailers closer to the consumer.

-

Faster, reliable service. If, and when, shipping becomes an “afterthought,” then e- commerce becomes a consumer habit, and market share increases. Unpredictable lead times are no longer acceptable.

2 Green Street Advisors.

Comparing the two types of retailers, it would seem that the omnichannel retailer should still have an advantage over the online retailer in availability if the omnichannel retailer is near the consumer.

Omnichannel retailers have a practically endless flexibility available for consumers. Consumers can go to a store and evaluate the options; they can buy in-store, or buy online. From there, consumers can have orders delivered from the store, or have the order shipped to another store for pick-up, or directly shipped to the home.

The options consumers enjoy when ordering from an omnichannel retail should give these companies tremendous competitive advantage over online retailers, whose customers’ only choices are to buy online and have orders delivered.

|

Online Retailer |

Omnichannel Retailer |

|

Advantages

|

Advantages

|

The online retailer’s competitive advantage is to offer faster delivery. That is the only way to effectively compete against the omnichannel retailer. As a result, omnichannel retailers must also offer similar flexibility in delivery services to meet the competitive pressures of the online retailer.

Driver: The Need for an Endless Aisle

The concept of an “endless aisle” has had longstanding interest with online retailers and omnichannel retailers. The trick is the technology backbone to make it work. Using the endless aisle model, retailers can reduce physical inventory, enhance the customer experience, and increase product assortment while decreasing floor space.

In many cases, retailers can arrange for manufacturers to drop ship. A drop ship strategy can also help to minimize risk with product obsolescence for short life span products.

Office Depot has created a virtual warehouse, which currently accounts for $500 million in revenue, and growing. The vendor receives daily feeds of inventory on-hand, and makes these products available to consumers online, where the supplier ships directly to the consumer.

Endless aisle is being embraced by retailers looking to increase revenue and marketshare. Retailers now have in-store computer terminals and kiosks that allow consumers to shop and purchase from a company’s full offerings. These kiosks have proven to be profitable. Smartphones and tablets are also being used by sales associates for ordering online, then using store pick-up or fulfillment.

Advantages to endless aisle3 include:

-

Provide customers a broad product selection.

-

Avoiding markdowns.

-

Increasing conversions and sales in stores.

-

Preventing sales losses.

-

Ensuring customer satisfaction.

-

Expanding offerings without space constraints.

-

Using e-commerce cross-selling and product recommendations.

-

Referring sales to partners.

-

Removing products from stores with low stock rotations.

Endless aisle is a driver for final delivery, and it will increase the volume of goods shipped directly to customers. As omnichannel retailers fully implement endless aisle, they close the gap on the competition from online retailers.

3http://digitalmarketing-glossary.com/What-is-Endless-aisle-definition

Driver: Movement to Quicker Fulfillment

When talking about the drivers of final delivery, the list must include the trend for same-day delivery by two retail titans: Amazon and Walmart. Because of the standard these two have set, consumers are coming to expect faster delivery to their doors for all items. Amazon is getting closer to its customer to reduce the time it takes to process and deliver orders.

Based on Tompkins International’s best estimates going forward, Amazon will grow from eight fulfillment centers (FCs) in 2004 to 54 FCs in 2014.

|

Date Range |

Total Sq. Footage of FCs that Amazon Built (in millions) |

Percentage of Total 2016 Sq. Footage |

Percentage Built per Year of Total 2016 Sq. Footage |

|

|

2002-2009 |

12.924 |

12.4% |

1.6% |

|

|

2010-2012 |

44.467 |

42.6% |

14.2% |

|

|

2013-2016 |

47.000 |

45.0% |

11.25% |

Amazon’s fulfillment centers tend to be 80-plus miles away from metro areas, so that they are closer to their customers to offer same-day delivery. In New York, for example, Amazon customers who order before 8:30 am will get delivery by 7 p.m.

What are consumers willing to pay for same-day delivery? Can retailers deliver at that price?

Among other examples of companies using quicker fulfillment is B&H Photo, which provides same-day pick-up in store.

This is similar to what Best Buy has offered in the past. A customer’s order is guaranteed to be available for pick-up in store or at a customer window at the DC or fulfillment center.

As a result of this competition from Amazon, Walmart’s response is to establish its own same- day delivery service. In a recent Walmart customer survey, the majority of respondents said they would consider same-day delivery if available, and more than half said they would use it monthly or more.

The survey found that electronics, toys, video games, movies, and groceries were among the items shoppers want delivered. The real questions are: What are consumers willing to pay for same-day delivery? Can retailers deliver at that price? The answer lies in delivery density.

In their current pilots, Walmart’s customers can place orders up until noon, and then they choose a four-hour window to receive the delivery the same-day. Walmart is using UPS delivery trucks to deliver the merchandise in select markets.

For the San Francisco and San Jose markets, shoppers have to order by 7 a.m. that day to receive those items. Walmart is using its own delivery trucks in those two regions.

Four Enablers of Final Delivery

The drivers of final delivery covered in this paper continue to increase the need for processes and service providers to meet consumer demands. Companies battling over the consumer dollar are continuing to increase competitive pressure for endless aisle and quicker fulfillment. The winners will be those that use the enablers to the full advantage. These four enablers are:

-

Network Design: Serving the customer base.

-

Order Management: Process time and visibility.

-

Store Fulfillment (omnichannel only): Inventory accuracy and how to cost-effectively pick from stores.

-

Regional Delivery: Quality delivery, on-time.

Enabler: Network Design — Getting the Right Mix

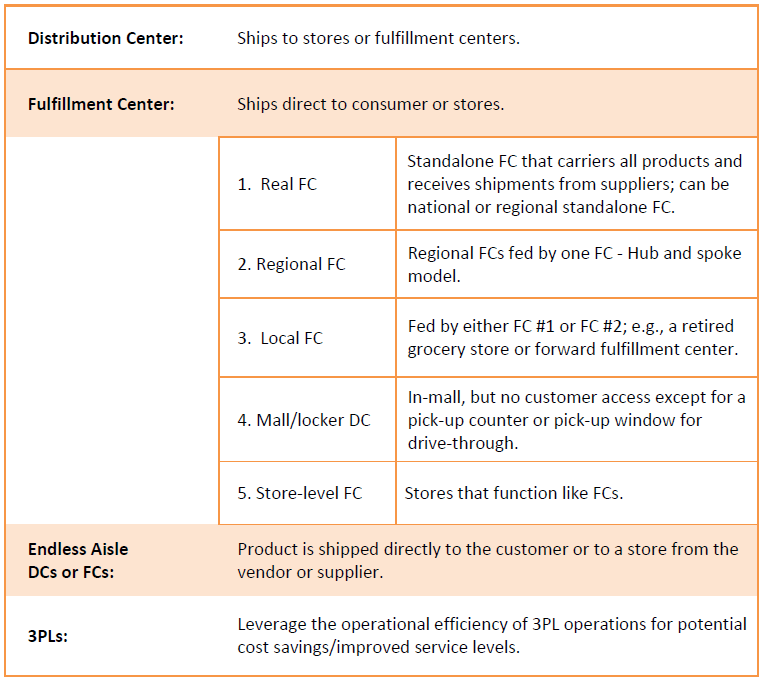

One consideration to get the right product to customers in the time frame they demand is network design. Retailers will have some combination of distribution centers, fulfillment centers, and drop ship vendors. To add to the mix, some have outsourced to 3PL providers.

It might make sense to put the DC and the FC in the same warehouse. As a result of evolving consumer preferences, the design needs to be flexible. In the past, network designs could be re-evaluated every three to five years.

Now, with changing supply chains, ideally the design should be reviewed every two to three years, with a focus on accurate forecasting and designs built on projected sales and marketing plans.

In the past, networks were designed while treating demand as independent of source. Today it is known that demand is dependent upon source, and so this must be built into the network design.

Below is a list of the options available to retailers. An expert evaluation will determine what you need:

Some big box retailers such as PetSmart have outsourced their whole online operations to a 3PL provider. The 3PL provider manages orders and is responsible for final mile delivery to the customer.

The challenge with 3PL providers is that the contracts must be taken into consideration with the overall network optimization. 3PL providers typically want a three to five-year commitment for their investments. This can be difficult to accept, due to the high level of uncertainty with future volumes and requirements.

The competitive landscape is changing. There is a better return on investment by leveraging technology to fulfill orders with as few moves as possible. Each company’s network must be designed to satisfy the strategy of the company.

Enabler: Order Management — DOM (Distributed Order Management)

Another key enabler is order management. Technology allows DOM to route an order to any DC, FC, store, or supplier. Based on inventory visibility, there needs to be a way to view the inventory across all facilities and route the order to the location closest to the customer. To take the order from the DOM, regional courier networks are becoming more sophisticated in their solutions (similar to FedEx or UPS).

Advanced carriers (LaserShip, DynaMex, OnTrac) can receive orders into their dispatching systems and capture delivery data for scalability.

Sample workflow for delivery:

-

Preferred & secondary courier providers are assigned zones around a location.

-

Order cut-off times and delivery promise dates established for each zone.

-

Capacity managed by carrier acceptance.

-

Customer alert features to provide delivery notices & exceptions.

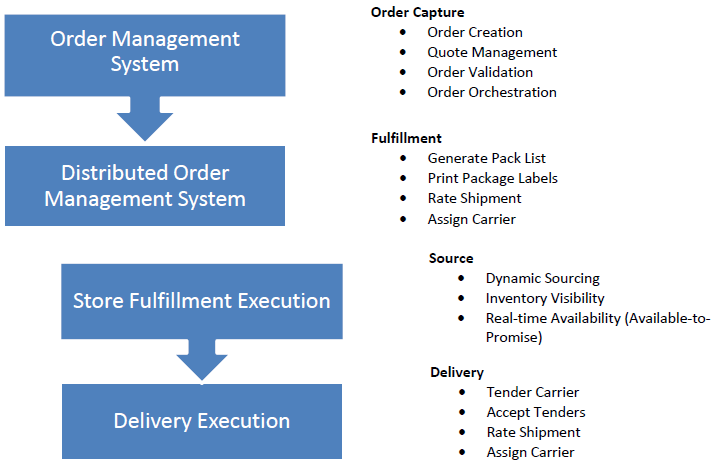

The diagram below shows a work flow from the order management system, to store fulfillment, to delivery execution.

The diagram shows how the order management system needs to connect to the store fulfillment system to execute the shipment and select the lowest cost carrier for a seamless customer transaction.

Enabler: Store Fulfillment Systems

Store fulfillment of customer-direct orders from retail stores will require automated systems. The orders can be generated from multiple sources (e.g. web storefront, call center, in-store systems).

They can be picked at an FC and dispatched to the store, picked from store backrooms, or picked from product on display to in- store customers. Customer orders can also be shipped directly to the home or shipped to another store for PUDO there or in lockers.

Store fulfillment system approaches are influenced by retailer type/size (e.g. big box, mall-based fashion chain, regional specialty), existing IT landscape (e.g. order management, retail inventory, web commerce, and store systems), and deployment model (e.g. pilot, interim, full production).

While they vary in functionality and scalability, an effective store fulfillment solution should provide:

-

A Seamless Experience for the Customer. Fulfillment from store (versus FC) should not appear any different from the customer’s perspective, regardless of how the order is entered (web store front, call center, in-store).

-

Integrated DOM / Order Brokering Backbone. Distributed order management and store fulfillment processes need to be tightly coupled, given the need to support hundreds of stores versus a handful of FCs. Issues and discrepancies need to be addressed in near real-time. Order brokering needs to dynamically account for variable store capacities and workloads. Orchestration between order brokering, store fulfillment and delivery services also becomes more dynamic, as delivery commitment moves towards next-day and same-day service.

-

Complete Inventory Visibility. Order management, order brokering and customer service need near real-time views of inventory availability across stores, as well as the entire distribution network. This includes inbound shipments and vendor-direct store deliveries.

-

Structure for Efficient Store Processes. As store fulfillment volumes increase, store associates need a seamless, single-execution system. This system needs to provide robust locator, workload management, pick/pack methods, and mobile functionalities.

Inventory Accuracy and Store Fulfillment

To date, there has been little need to invest in warehouse-grade inventory tracking/visibility at the shelf level. The technology is available with RFID. Retailers have been evaluating RFID for some time and unwilling to make the investment. RFID is an option to solve inventory accuracy issues for the fulfillment of orders for products on display to in-store customers.

One thing for certain is that retailers will need to consider the technical and operational challenges related to improving store-level inventory accuracy. Accuracy of inventory products on display to in-store customers is often 60-80 %, and this picking from display inventory is really only usable on ‘save a sale’ type circumstances.

Enabler: The Final Delivery Service Provider — Local, Regional, National

The new e-commerce model has introduced new delivery requirements for rapid service from any supply point to customer homes, businesses, or other pick-up points. Rapid delivery is a critical customer service benefit desired by companies to increase market share. Delivery examples include the following:

-

Amazon offers Prime members free 2-day delivery for a yearly subscription fee. Tompkins International believes this will go to next-day delivery by the end of 2015.

-

LaserShip is piloting same-day delivery in NY, Philadelphia, and Boston for Amazon and Barnes & Noble.

-

DynaMex is testing same-day delivery with Sears in Chicago.

-

Amazon and WalMart offer service to store-based lockers for customer pick-up.

These specialized services are provided by a highly fragmented, evolving supply base. Service providers for the final delivery market are dominated by FedEx, UPS and USPS, with the remainder of the market highly fragmented and regional.

The market for residential and business final delivery is growing rapidly as a result of online ordering and direct- to-customer markets. Revenues in these sectors are growing at 5-10% per year.

Final delivery service levels are same-day, next-day, second-day and ground. The regional same- day and next-day delivery market includes hundreds of small, independent businesses serving regional areas and a small number of multi-location regional or national operators. Tompkins International estimates the residential and business parcel delivery market in the US is approximately $100 billion. Regional parcel carriers are growing, and generally offer lower prices than nationals. Amazon has switched many areas to regional carriers in an effort to lower cost.

Aggregators are forming, combining independents into larger virtual carrier services. Aggregators include companies such as 1800Courier, Shutl and Courierboard.com. Courierboard.com is designed to bring individuals, shippers, and companies with shipments together on a website with professional courier companies throughout the U.S. The site operates as a bid-based system. Couriers respond with a bid to provide delivery of a posted shipment. Companies and individuals with shipments can post their delivery quote requests and delivery RFPs on Courierboard for free.

Shutl, founded in the UK in 2008, is a software company that coordinates orders with local retailers and courier companies. Shutl is working with regional retailers to launch its service in San Francisco, Chicago and New York with 17 additional markets to follow over the next year. Shutl aggregates couriers throughout the US to provide a national solution for retailers. Service is only available for omnichannel retailers within 10 miles of a customer’s home. It offers online shoppers the choice to have orders delivered within 90 minutes of purchase, or to choose a one-hour delivery window that same day (or any day). Shutl has already indicated they will not work with Amazon, because they compete with their customers.

A third company, 1800Courier, provides same-day courier solutions to consumers, and it has over 1500 active clients. Started in 1997, 1800Courier contracts with courier service providers in the US. As an example of current volume, 1800Courier serves the Chicago metro area with approximately 300-400 deliveries per week.

Same-day service is a unique business model as supplied by courier services. These companies do not operate a large capital-intensive national hub network like FedEx or UPS. The companies range from local fleet providers with minimal terminal requirements to regional or national providers with variety of sort/segregate networks. These and other carriers are rapidly evolving to service this emerging need by:

-

Creating dispatch and track & trace systems for scalability and consumer use.

-

Expanding their locations and service territories.

-

Expanding their contractor relationships with various specialized players.

-

Engaging in pilot tests with retailers.

-

Subcontracting to FedEx and UPS for delivery in less-served regions.

Carrier capabilities vary dramatically. The marketplace can be categorized in three significant ways:

-

Time versus delivery capability; with delivery capability being a function of the underlying network model.

-

Time: Same-day, versus next-day, and versus longer time frames.

-

Type of merchandise delivered: Parcel-type versus larger and/or unusual shapes, usually with customized services like installation assistance.

-

-

Systems capability.

-

Ownership model: Use of internal, versus independent contractor, versus aggregator models.

Those in final delivery services are playing an escalating role in buying and distribution changes in various industries. Retailers, consumer product companies, endless aisle suppliers, and distributors are all increasingly considering local and regional service providers as a way to cut costs and improve service.

Evidence of this change includes the following.

-

Over 60% of independent courier service companies cater to the retail market. A 2012 survey indicated that no independent couriers cited this as an industry they supported as recently as 2010.4

-

Couriers are increasing their capabilities in their operations efficiency, including standard operating procedures, dispatch operations, claims management, workforce issues, security, fuel surcharge programs, and back office routing solutions.

-

As a result of software companies such as CXT, Vendornet, Datatrac, and others, regional players can offer the same product tracking and capabilities of a UPS or FedEx.

-

Regional carriers can offer a more flexible, cost-effective delivery service.

Traditional home delivery companies such as Amway have established a parcel bid process by region, and consider it a core competency to reduce their $140M in transportation spend.

-

Amazon has embraced the use of regional couriers, including Ontrac and Lasership; Tompkins International research indicate they pay approximately $4 / package for final delivery.

There are an estimated 7,000 regional carriers in the US.5 Most of them serve local cities. Regional carriers can offer a more flexible, cost effective delivery service when compared to UPS or FedEx. This is because regional providers offer the latest pick-ups and earliest deliveries and can often provide faster delivery within regions.

Also, a consumer can get more attention from regional providers. In terms of cost benefits, the discounts can be better for medium-size clients, and there are typically fewer accessorial charges. Some offer residential delivery at no charge.

Final delivery service providers can market several different shipment service offerings.

4http://www.mcaa.com/Portals/0/News Releases/Survey Results 2012 Release.pdf

5http://www.mcaa.com/IndustryResources/IndustryProfile/tabid/186/Default.aspx

-

Expedited: Orders delivered same-day or next-day.

-

Time Sensitive Deliveries: Orders required to be delivered within a timed window.

-

Vendor Pick-up: Trailer availability to leave at a warehouse to be loaded and brought back to a main sort center within that region.

-

Routed: Dedicated driver picks up and delivers all orders on a daily route.

-

Sort and Delivery: Receive linehaul goods to warehouse and sort for final delivery.

-

Forward Stocking and Delivery including Lockers: Forward stocking of frequently- purchased items across regions, available same-day or next-day for local consumers, can maintain or exceed shipper service level agreements.

-

Reverse Logistics: Reverse logistics can be provided in conjunction with delivery services or as a standalone service, with the greatest demand from the internet retailing sector.

Companies that have established themselves profitably in the final delivery space have leveraged competitive advantages. They gain market share from FedEx and UPS, because of their flexibility and willingness to provide services that UPS or FedEx will not, or cannot. The companies often start small. They then add value-added services and build their relationships with consumers and additional geographies.

No two regional courier services offer the same value-added services. They are dependent on how relationships evolved with their customers. Value-added services can differ significantly among customers, and they are a matter of understanding their supply chain issues and how companies can help solve them.

Conclusion

The ability for companies to gain market share requires that customer shipping become convenient, simple, reliable, and inexpensive. The current state of the industry calls for these capabilities:

-

Development of a business strategy with specific delivery service time requirements defined. Leaders are well engaged on this front. Laggards not so, with a serious threat of bankruptcy without change.

-

Estimating the cost, and profitability, of achieving the desired service levels. This is less developed than the business strategy. The fragmented carrier base and wide variations in rates is problematic, particularly with next-day and same-day delivery. Many companies are undergoing pilots to understand the space better and develop their responses.

-

The issue with time-critical delivery is density. Carriers are finding that density with individual company networks can be cost-prohibitive.

-

Source and manage a non-traditional carrier base aligned to the capability and time- critical service level niches defined in the business plan. Companies are researching carrier capabilities on an opportunistic basis.

Leaders are developing, although it is slow-going. Omnichannel retailers, consumer product companies doing retail, endless aisle providers, and distributors need a strategic roadmap to determine how to leverage competitive advantages.

An effective roadmap will take into account the drivers and enablers of final delivery, as well as the new retail model, which both are outlined in this paper. There is no one-size-fits-all solution, as the plan also must account for network design, forecasted e-commerce growth, order-to-delivery service levels, and how to implement at the lowest possible cost/fewest moves with seamless customer interfaces. But the leaders who act now and use the process of final delivery’s full potential will move far ahead of the competition.

About Tompkins International

Tompkins International transforms supply chains to help create value for all organizations. For more than 35 years, Tompkins has provided end-to-end solutions on a global scale, helping clients align business and supply chain strategies through operations planning, design and implementation. The company delivers leading-edge business and supply chain solutions by optimizing the Mega Processes of PLAN-BUY-MAKE-MOVE-STORE-SELL. Tompkins supports clients in achieving profitable growth in all areas of global supply chain and market growth strategy, organization, operations, process improvement, technology implementation, material handling integration, and benchmarking and best practices. Headquartered in Raleigh, NC, USA, Tompkins has offices throughout North America and in Europe and Asia. For more information, visit www.tompkinsinc.com.

|

Follow Tompkins International: |

Visit our YouTube channel to view these videos and more from Tompkins International.

The Amazon Cure to the Plague of Short-Term Thinking in Business